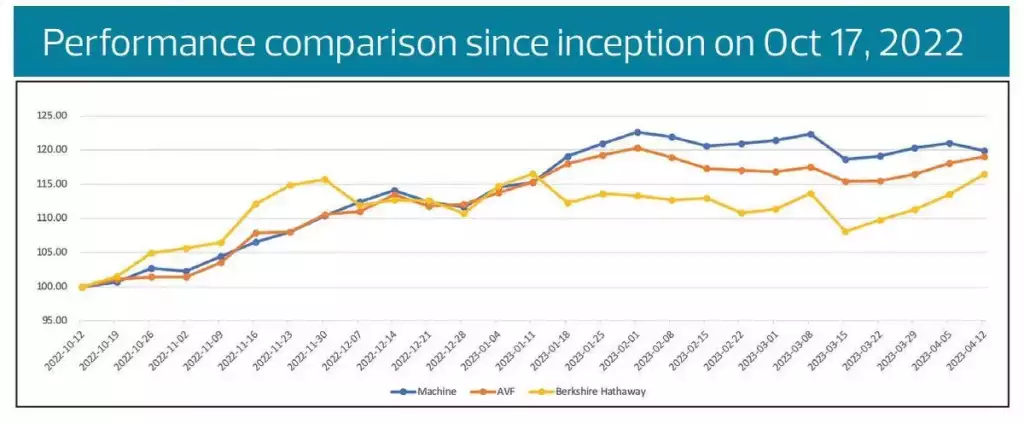

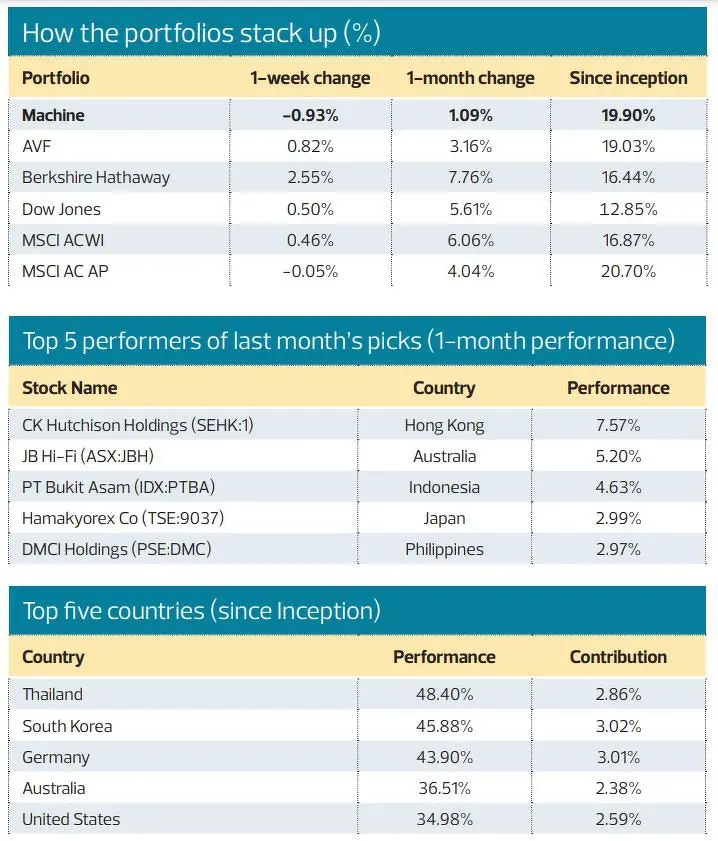

Deep Deep faces its first mini black swan event and still triumphs. On a monthly basis, the Deep Deep portfolio lost out to Aggregate Value Fund (AVF), Berkshire Hathaway and the benchmark indexes. Deep Deep was up 1.1% for the past month. The primary cause was the recent US banking crisis which triggered a massive sale of US banking stocks.

Our US pick, Home Bancorp, fell 9.9% during our holding period over the past month. However, this drop was cushioned by 14 other stocks in the portfolio. The good news is that since the inception of the Machine versus Man competition, the Deep Deep portfolio has won most competing portfolios and indexes by gaining 19.9%. Deep Deep is still ahead of the pack.

This month, we bought Wajax Corporation, Alliance Global Group, Sempio Company, Tyman, Huntsman Corporation and Bai Sha Technology. Conversely, we sold Algoma Central Corporation, Central Asia Metal, Home Bancorp, DMCI Holdings, SNT Motiv and Asia Cement Corporation.

Our first mini-black swan event

The collapse of Silicon Valley Bank and the subsequent contagion effect was unexpected. We call this a mini–black swan event. While Home Bancorp, which was in our 15 picks, was not one of the US regional banks that suffered a run, or was at risk of a run, it has nonetheless suffered from collateral damage as investors fled from these stocks.

The lesson here, as we have said many times in this column, is that Deep Deep is a probabilistic AI. It does not foretell the future. AI cannot predict black swan events because there are insufficient data on such events for the AI to learn. Nassim Nicholas Taleb, the author who made this term famous, once said, “The problem with (human) experts is that they do not know what they do not know.”

In the AI context, it can be rephrased as “The problem with AI is that it cannot predict what it did not learn”. The good news is that there are 15 shares in the Deep Deep portfolio, and they collectively cushioned the devastating falls of a few picks.

Another valuable lesson worth noting is that Deep Deep is an extreme implementation of an AI-powered portfolio. As explained in January, the margin of safety is to have at least five stocks per country, amounting to 15*5=45 stocks in the Deep Deep portfolio. There is simply insufficient space to list all these stocks in this column so we settled with 15.

Eric Kong, our fund manager and Deep Deep developer, felt that 15 stocks would be testing the extreme limits of Deep Deep’s abilities. He reasoned that if Deep Deep can deliver an outstanding result in this competition with only 15 stocks, then our actual implementation in Aggregate’s AVF portfolio will be even safer. In this case, the 15 stocks portfolio demonstrated the power of diversification. In start-up speak, our Minimum Viable Product (MVP) works!

Why can’t you duplicate Deep Deep results in AVF now?

Size matters A few readers including our clients at Aggregate Asset Management asked us this question — if Deep Deep portfolio can deliver such spectacular results why can’t the Aggregate fund managers convert their funds, the AVF, and the Aggregate Global Equities Fund, to a Deep Deep-like portfolios and earn similar returns?

The answer is simple. Firstly, the good news is that since last year, we have already started the process of transforming our two funds into AI-powered funds. Since the start of the Machine versus Man competition, AVF has delivered 19.03% returns, versus its benchmark MSCI AP’s 20.70%. Against the backdrop of a choppy global stock market, the results are indeed stunning.

Secondly, we must understand the relative size between Deep Deep’s portfolio and AVF. The Deep Deep portfolio started at US$500,000 ($663,518), while AVF is about $500 million, or US$376 million. Size matters in portfolio management. In an equally weighted Deep Deep portfolio with 15 stocks, we would allocate about US$33,800 in each stock.

On the other hand, we have 1,500 stocks in the AVF portfolio, resulting in a theoretical average of US$238,000 allocation per stock. It will take more than a week to fulfil a buy/sell order for each stock in AVF. Now multiply that by 1,500 stocks and you see the complexity of the transformation.

Visually, think of big, monstrous vessels like the Titanic trying to avoid the iceberg. Had the Titanic been a much smaller and nimbler ship, James Cameron would have had to film a happy ending for Leonardo Di Caprio, who then might be shown dry, but as wrinkled as Rose. For those who love sci-fi, think of the Imperial Star Destroyer versus Han Solo’s Millennium Falcon.

Interestingly, Warren Buffett said the same. “Size is the enemy of performance. You cannot move a big ship quickly, and you cannot beat the market by being like the market.” Essentially, Buffett has compared managing a large fund to steering an oil tanker, saying that it is much more difficult to change course quickly and that the fund’s size can limit its agility and flexibility.

Human versus Machine – a lesson from AlphaGo

One of our investors asked, “Do the quant team in Aggregate gleefully celebrate every month when you beat the human portfolios and the competing benchmarks?” The answer is no.

I started my career in the financial industry as an intern equity analyst in a local stock brokering firm and I know how difficult it is to analyze a stock and ultimately make a buy/sell recommendation. It is hard work. It is a job that humbles you when you grow egoistical and yet occasionally rewards you for having the guts to stand by your convictions. Those with weathervane-like or suck-up-to-your-superior characteristics should avoid this industry.

It is with such a backdrop that I re-watched the award-winning documentary AlphaGo recently. It is about a group of Google programmers using AI to beat a South Korean Go world champion, Lee Sedol. Lee started the competition by dismissing his AI competitor politely but ended up in tears when he lost four games out of five to AlphaGo. The horror slowly dawned on him and the global Go community that no human will ever beat the AI.

Contrast this to the Google team which looked like a bunch of precocious geeks from Revenge of the Nerds, high-fiving each other. Yet, in that single game in which Lee Sedol beat the AI, you could see the paradoxical reaction from the Google team — they were relieved that a human could still win.

The Aggregate team carries the same matured perspective. We are proud of Deep Deep’s accomplishments but we see it as a tool that greatly enhances our stock-picking process and not as a master that overrides human ingenuity. We are chill about its outcome. We don’t high-five. We are humans after all.

Harry Huo is head, special projects, at Aggregate Asset Management.

This article is a product advertisement. The Edge does not directly or indirectly make any endorsement and cannot verify the performances of the Deep Deep Machine Fund, which we understand is not an independent, dedicated, segregated fund. The Deep Deep Portfolio’s US$500,000 capital is a part of the AVF fund, which is, in turn, a part of Aggregate Asset Management’s AUM of approximately $550 million. While the AVF fund is audited yearly by EY and reports to MAS, this does not mean that the Deep Deep Portfolio is independently audited.

To view all articles in the Man vs Machine Challenge series, please click here.

This article was published on The Edge Singapore on 17 April, 2023.