We are 10 months into the competition, having clocked nearly 300 days. And we have beaten everyone and every index except Warren Buffett.

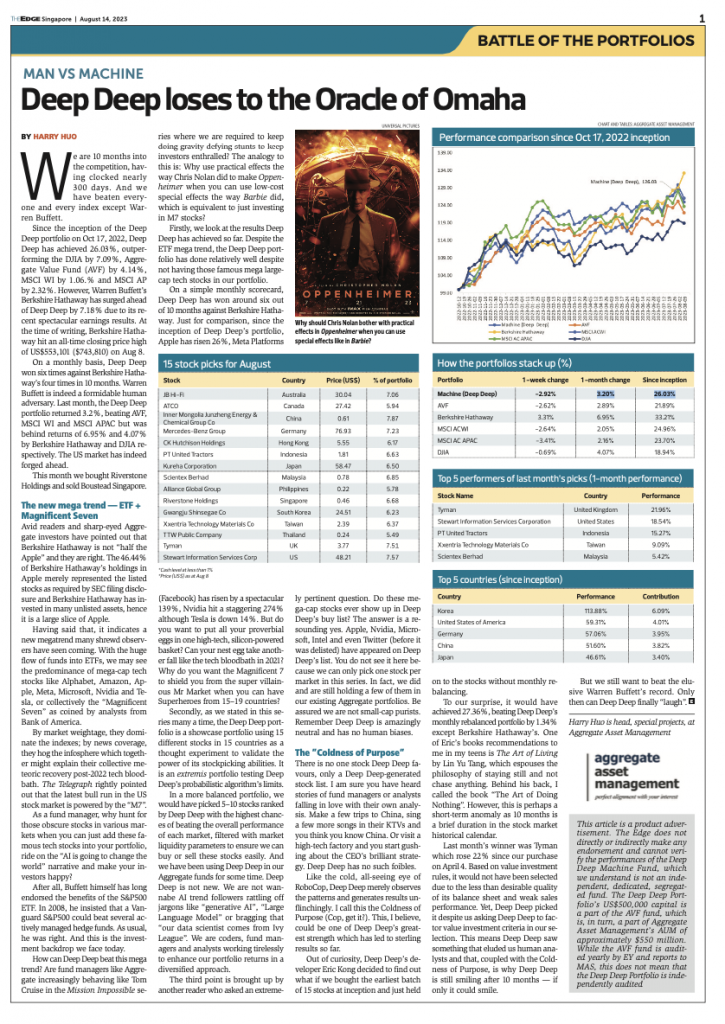

Since the inception of the Deep Deep portfolio on Oct 17, 2022, Deep Deep has achieved 26.03%, outperforming the DJIA by 7.09%, Aggregate Value Fund (AVF) by 4.14%, MSCI WI by 1.06.% and MSCI AP by 2.32%. However, Warren Buffett’s Berkshire Hathaway has surged ahead of Deep Deep by 7.18% due to its recent spectacular earnings results. At the time of writing, Berkshire Hathaway hit an all-time closing price high of US$553,101 ($743,810) on Aug 8.

On a monthly basis, Deep Deep won six times against Berkshire Hathaway’s four times in 10 months. Warren Buffett is indeed a formidable human adversary. Last month, the Deep Deep portfolio returned 3.2%, beating AVF, MSCI WI and MSCI APAC but was behind returns of 6.95% and 4.07% by Berkshire Hathaway and DJIA respectively. The US market has indeed forged ahead.

This month we bought Riverstone Holdings and sold Boustead Singapore.

The new mega trend — ETF + Magnificent Seven

Avid readers and sharp-eyed Aggregate investors have pointed out that Berkshire Hathaway is not “half the Apple” and they are right. The 46.44% of Berkshire Hathaway’s holdings in Apple merely represented the listed stocks as required by SEC filing disclosure and Berkshire Hathaway has invested in many unlisted assets, hence it is a large slice of Apple.

Having said that, it indicates a new megatrend many shrewd observers have seen coming. With the huge flow of funds into ETFs, we may see the predominance of mega-cap tech stocks like Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla, or collectively the “Magnificent Seven” as coined by analysts from Bank of America.

By market weightage, they dominate the indexes; by news coverage, they hog the infosphere which together might explain their collective meteoric recovery post-2022 tech bloodbath. The Telegraph rightly pointed out that the latest bull run in the US stock market is powered by the “M7”.

As a fund manager, why hunt for those obscure stocks in various markets when you can just add these famous tech stocks into your portfolio, ride on the “AI is going to change the world” narrative and make your investors happy?

After all, Buffett himself has long endorsed the benefits of the S&P500 ETF. In 2008, he insisted that a Vanguard S&P500 could beat several actively managed hedge funds. As usual, he was right. And this is the investment backdrop we face today.

How can Deep Deep beat this mega trend? Are fund managers like Aggregate increasingly behaving like Tom Cruise in the Mission Impossible series where we are required to keep doing gravity-defying stunts to keep investors enthralled? The analogy to this is: Why use practical effects the way Chris Nolan did to make Oppenheimer when you can use low-cost special effects the way Barbie did, which is equivalent to just investing in M7 stocks?

Firstly, we look at the results Deep Deep has achieved so far. Despite the ETF mega trend, the Deep Deep portfolio has done relatively well despite not having those famous mega large-cap tech stocks in our portfolio.

On a simple monthly scorecard, Deep Deep has won around six out of 10 months against Berkshire Hathaway. Just for comparison, since the inception of Deep Deep’s portfolio, Apple has risen 26%, Meta Platforms (Facebook) has risen by a spectacular 139%, Nvidia hit a staggering 274% although Tesla is down 14%. But do you want to put all your proverbial eggs in one high-tech, silicon-powered basket? Can your nest egg take another fall like the tech bloodbath in 2021? Why do you want the Magnificent 7 to shield you from the super villainous Mr Market when you can have Superheroes from 15–19 countries?

Secondly, as we stated in this series many a time, the Deep Deep portfolio is a showcase portfolio using 15 different stocks in 15 countries as a thought experiment to validate the power of its stockpicking abilities. It is an extremis portfolio testing Deep Deep’s probabilistic algorithm’s limits.

In a more balanced portfolio, we would have picked 5–10 stocks ranked by Deep Deep with the highest chances of beating the overall performance of each market, filtered with market liquidity parameters to ensure we can buy or sell these stocks easily. And we have been using Deep Deep in our Aggregate funds for some time. Deep Deep is not new. We are not wannabe AI trend followers rattling off jargons like “generative AI”, “Large Language Model” or bragging that “our data scientist comes from Ivy League”. We are coders, fund managers and analysts working tirelessly to enhance our portfolio returns in a diversified approach.

The third point is brought up by another reader who asked an extremely pertinent question. Do these mega-cap stocks ever show up in Deep Deep’s buy list? The answer is a resounding yes. Apple, Nvidia, Microsoft, Intel and even Twitter (before it was delisted) have appeared on Deep Deep’s list. You do not see it here because we can only pick one stock per market in this series. In fact, we did and are still holding a few of them in our existing Aggregate portfolios. Be assured we are not small-cap purists. Remember Deep Deep is amazingly neutral and has no human biases.

The ”Coldness of Purpose”

There is no one stock Deep Deep favours, only a Deep Deep-generated stock list. I am sure you have heard stories of fund managers or analysts falling in love with their own analysis. Make a few trips to China, sing a few more songs in their KTVs and you think you know China. Or visit a high-tech factory and you start gushing about the CEO’s brilliant strategy. Deep Deep has no such foibles.

Like the cold, all-seeing eye of RoboCop, Deep Deep merely observes the patterns and generates results unflinchingly. I call this the Coldness of Purpose (Cop, get it?). This, I believe, could be one of Deep Deep’s greatest strength which has led to sterling results so far.

Out of curiosity, Deep Deep’s developer Eric Kong decided to find out what if we bought the earliest batch of 15 stocks at inception and just held on to the stocks without monthly rebalancing.

To our surprise, it would have achieved 27.36%, beating Deep Deep’s monthly rebalanced portfolio by 1.34% except Berkshire Hathaway’s. One of Eric’s books recommendations to me in my teens is The Art of Living by Lin Yu Tang, which espouses the philosophy of staying still and not chase anything. Behind his back, I called the book “The Art of Doing Nothing”. However, this is perhaps a short-term anomaly as 10 months is a brief duration in the stock market historical calendar.

Last month’s winner was Tyman which rose 22% since our purchase on April 4. Based on value investment rules, it would not have been selected due to the less than desirable quality of its balance sheet and weak sales performance. Yet, Deep Deep picked it despite us asking Deep Deep to factor value investment criteria in our selection. This means Deep Deep saw something that eluded us human analysts and that, coupled with the Coldness of Purpose, is why Deep Deep is still smiling after 10 months — if only it could smile.

But we still want to beat the elusive Warren Buffett’s record. Only then can Deep Deep finally “laugh”.

Harry Huo is head, special projects, at Aggregate Asset Management

This article is a product advertisement. The Edge does not directly or indirectly make any endorsement and cannot verify the performances of the Deep Deep Machine Fund, which we understand is not an independent, dedicated, segregated fund. The Deep Deep Portfolio’s US$500,000 capital is a part of the AVF fund, which is, in turn, a part of Aggregate Asset Management’s AUM of approximately $550 million. While the AVF fund is audited yearly by EY and reports to MAS, this does not mean that the Deep Deep Portfolio is independently audited.

To view all articles in the Man vs Machine Challenge series, please click here.

This article was published on The Edge Singapore on 10 August, 2023.