31 December 2021

NAV per Share SGD: 191.07

Fund Size: SGD 553M

Dear Investor,

We did well in 2021. It was a record year. The AVF delivered +18.26% nett of all fees to investors. In contrast, the benchmark index, the MSCI AC Asia Ex Japan suffered a -4.72% loss. We outperformed the index by +22.98%.

The MSCI AC Asia Ex Japan’s poor performance was caused by China’s slowing growth, property sector jitters and the Government regulatory crackdowns on the tech sector. For example, Tencent Holding’s share price declined by -20%, Alibaba Group by -50% and China Evergrande by -90%.

The reason we avoided the blow-ups is because of our extensive diversification and us maintaining the discipline in not taking huge bets in a few companies. As a matter of fact, we hold 1540 stocks spread across 13 countries at the end of 2021. Our top 5 positions only constitute 2.4% of our portfolio.

In 2021, the strength of our process shows itself – we delivered stellar performance despite being extremely diversified. We believe that investing in stocks is a long game, and to win, we must not make any major mistakes. We believe that if we manage risk carefully, and in a disciplined fashion, the results will be decent in the long-term through compounding effects.

We have read about a famous and talented fund manager that put 15% of their investor’s funds in Tesla. If the manager is right, good for him/her and his/her investors. These are called high-conviction investing – where large sums of money are put into the best ideas. We don’t do that – firstly because we are not talented, and secondly, most of our investors are retirees with a major portion of their net worth with us and we don’t think we should subject them to that kind of excitement.

Today, people are concerned about inflation and rising interest rates. (If I remember correctly, there was no period in the last 100 years where people were not concerned about anything. 10 years ago, it was deflation, now it’s inflation, and sometime in between, stagflation, with a dash of depression thrown in occasionally for good measure).

If you know us well, you will know that we are proponents of an all-equity portfolio. This means that we think that people should put as much money as they can in stocks. History tells us that the best performing asset class is stocks. Of course, stock fluctuations can be frightening, as we all know, but somehow, we got to steel ourselves if we want to maintain the purchasing power of our money.

Why do we keep saying that stocks are best?

When you buy a stock, you are buying a small share of a business. Some businesses can pass on inflationary costs to their customer, and some can’t. But overall, if you average out all the businesses in the world, businesses earn 10% on capital in the last 100 years. This means that if you put $1 in a business, you will earn 10 cents on average. (This is called the Return on Equity, or ROE). Of course, the ROE fluctuates year to year, and it also depends on the company’s usage of debt. During the pandemic, ROEs took a hit and drop to single digits, and in the recent recovery, ROE will once again surpass the 10%. Businesses in different countries have different ROE as well. In the USA, ROEs are in the mid-teens, 12-15% on average, and in China, it used to be 15%-17% but in the last 5 years have dropped to 7-8%. Singapore businesses have ROEs of 5-7% in the last few years, but during their halcyon years in the 90s to 2000, they enjoyed ROEs of 15% and upward. Singapore companies’ lacklustre single-digit ROEs in the last 10 years have explained the poor performance of the Singapore stock market. (The STI index is always at 3200).

No matter how you look at it, somehow, the long-term average ROE always hovers around 8-10% globally. And it is this figure that drives the long-term returns of the stock market

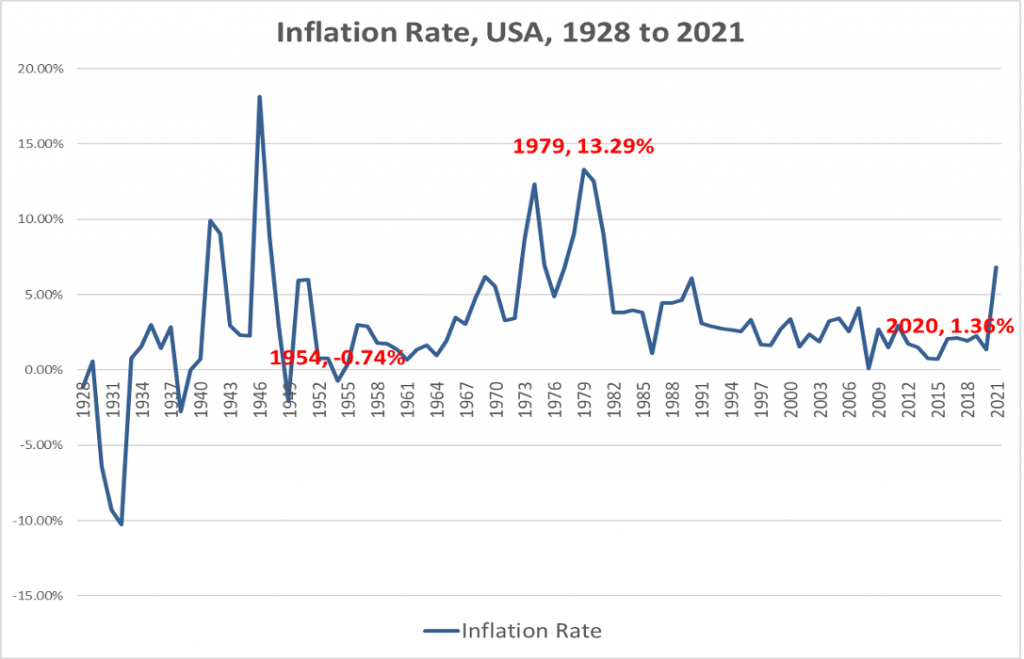

Let’s examine inflation rates from 1928 to 2021 in the USA. See Chart A.

There are distinctly 2 periods:

From 1954 to 1979 we had rising inflation and increasing interest rates. Inflation rose from -0.74% in 1954 to 13.29% in 1979.

From 1980 to 2021 we had declining inflation and reducing interest rates. Inflation declined from a high of 13.29% in 1979 to 1.36% in 2020.

So, how did the different asset classes perform during each of this period – one with rising inflation from 1954 to 1979, and the other with declining inflation from 1980 to 2021? See Table B.

Chart A

Table B

Stocks performed well for both periods – handily beating bonds and real estate. Note that the average annual returns from stocks (7.42% to 9.77%) mirror the average historical ROEs.

Bonds benefited in the last 40 years, from 1980 to 2020 when interest rates trended lower, returning 4.80% p.a. real returns. However, if interest rates go up, we can expect bonds to perform poorly, as evident from 1954 to 1979, where real returns for bonds were negative.

Real estate returned low single digits for both periods. This might surprise Singapore property investors. Remember that this is the US market, and not Singapore, Hong Kong or London, where real estate is at a premium.

So, if the investor is thinking of reducing his equity exposure because of the impending interest rate rise, do not forget the superior performance of stocks over all periods.

“How are we going to position our portfolio for inflation?”

We will do the obvious – interest rate increases will punish firms with a lot of debt. So, we will avoid those. Actually, we have been avoiding companies with weak balance sheets all the time. The AVF portfolio has a Net Debt/Equity ratio of 5% and a current ratio of 1.8X – which is considered sound.

Eric Kong

Aggregate Asset Management